Dame Judith Hackitt was awarded an honorary fellowship at the RIBA last month. Now a household name within the construction industry, the impact of her report ‘Building a Safer Future’ has been profound: it is no overstatement to suggest that the new Building Safety Act, which came into force this month, is built almost entirely on her recommendations.

The speed of her work was astonishing. Instructed on 30 August 2017, a mere 11 weeks after the fire at Grenfell Tower, Dame Judith published her interim report on 18 December 2017 and her final report on 17 May 2018 – an incredible achievement.

Another, in my view equally important, report was instructed in April 2021 by the Ministry of Housing, Communities and Local Government (MHCLG). Led by Paul Morrell (ex-senior partner of Davis Langdon Everest Cost Consultants) and King’s Counsel Anneliese Day, ‘Testing for the Future’ was finally published by the Department for Levelling Up, Housing and Communities (DLUHC) on 23 April 2023 – rather mysteriously a good 18 months after its completion. An obvious complement to the Hackitt Report’s focus on Building Regulations and Fire Safety in terms of statutory controls and design, this second report has investigated the territories of product testing, certification, and representation through trade literature – another world of astonishing mystery and confusion.

Despite Morrell’s thorough understanding of the UK’s extraordinarily fragmented construction industry, he must surely have benefited enormously from the partnership with KC Day who was recently described in language not common to her profession as “an absolute Rockstar at the top of her game”. Praise indeed for someone who, in 2020, was named ‘International Arbitration Silk of the Year’ having previously been shortlisted as ‘Professional Negligence Silk of the Year’, named ‘Construction and Energy Silk of the Year’ three times, and ‘Barrister of the Year’ in 2014 by The Lawyer.

The Morrell-Day report should have an impact on the construction industry just as profound as that of Judith Hackitt, for whilst Hackitt has laid bare the confused complexity and ambiguity of a regulatory process which she described as ‘not fit for purpose’, Morrell and Day have opened the lid on a pandora’s box of misrepresentation and deception. They have also drawn attention to the extraordinarily fragmented nature of our industry which the following image listing the members and associate members of the Construction Industry Council (CIC), illustrates only too well:

Apparently, British construction is represented by over 500 institutes, guilds, confederations, and the like….

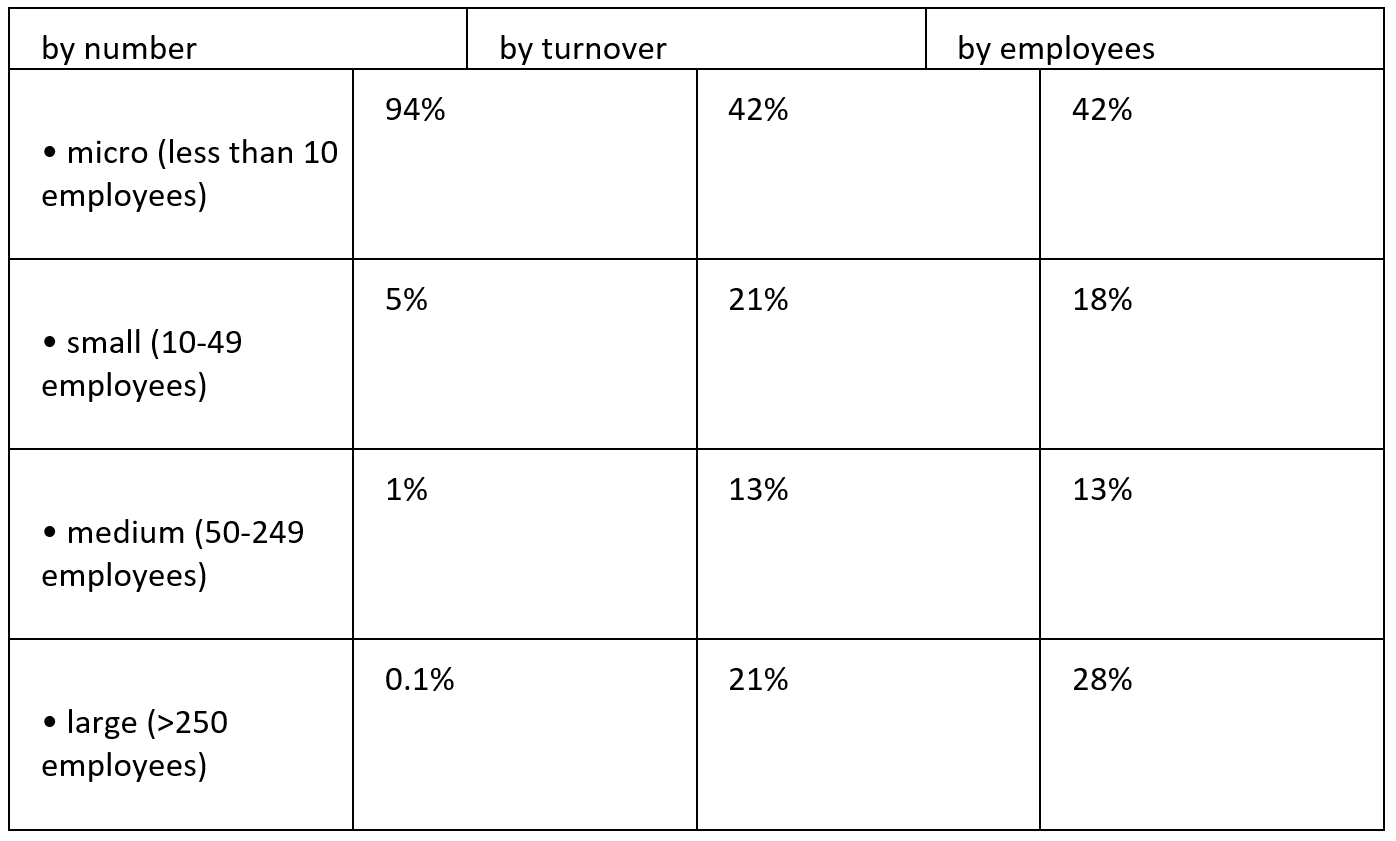

In a fascinating early section of their report entitled ‘Mapping the Landscape’ Morrell and Day illustrate this fragmentation by reporting that in 2019 the ‘headline statistics’ across the entire UK industry – that is contracting, professional services, and product manufacturing – were:

- total UK turnover: £432bn, representing 8.8% of UK Gross Domestic Product (GDP).

- number of firms: 407,754

- number of people employed: 2,243,000 (plus 843,000 self-employed, primarily in contracting)

- size distribution of firms:

It is not difficult to see that that such fragmentation has obvious and very serious implications with respect to regulation, control, quality and, in consequence, the safety of our buildings. Indeed, in a somewhat chilling passage of the report the authors describe in detail the realities of the industry’s trading conditions and the business models by which it operates in response to the forces of demand and supply:

……these forces, which have been the subject of constant studies, do not excuse the inexcusable: incompetence should not be tolerated, and there should be no hiding place for misconduct. They do, however, mean that propositions for change, including the expectation of a change of culture, are likely to succeed only if they are rooted in an appreciation of the powerful business drivers that the industry’s operating model responds to.

These drivers and operational responses can be summarised as follows:-

(1) a pattern of demand that is both diverse (from small refurbishment projects to huge new build infrastructure) and volatile (as the capital investment tap is turned on and off in response to economic cycles), compounded by constant bespoke variation of clients’ requirements;

(2) an industry that is consequently reactive, waiting for the next enquiry before equipping itself to respond;

(3) fragmentation within the industry, both in terms of the number of businesses and the way it organises itself, with fractures between design and construction management, between the management of construction and its execution, and between those who design and construct buildings and those who occupy them – with the critical consequence that nobody owns the whole process;

(4) an industry that is not dominated by a small number of major players in the same way as more concentrated industries (the turnover of the largest UK contractor is about 15% of the turnover of the largest supermarket, and the market share of the top 5 contractors is less than 20%, compared with more than 60% for the top 5 supermarkets);

(5) a high dependence upon subcontracting;

(6) a highly mobile workforce, with a high proportion of self-employed (and, to date, a significant proportion of migrant labour), so investment in training is a particular casualty of market failure;

(7) relatively low barriers to entry, with working capital largely provided by the industry’s customers;

(8) notwithstanding low barriers to entry, relative protection from the high levels of foreign competition that have transformed other industries;

(9) low levels of innovation, including slow take-up of industrialisation and digitalisation;.

(10) a limited understanding and appreciation of how built assets actually create value, on the part of both the demand and supply sides, with the result that lowest initial cost becomes the principal driver;

(11) consequently high levels of competition at low margins, often in the expectation that a margin can be created or increased by “playing” the terms of contract later, by driving down suppliers’ prices, or by product substitution;

(12) the consequent prevalence of opportunistic tendering within the supply chain, rather than the assembly of a settled team that can strive for continuous improvement;

(13) the absence of a feedback loop by which learning can be collected and disseminated; and

(14) low levels of independent oversight of quality assurance and compliance.

Make no mistake, this is sobering stuff which well illustrates the challenges we face in, for example, matching up to the performance and safety standards which are achieved within aviation design, production, operation and maintenance.

The authors concluded this part of their report with the observation that:

……..to the extent that a whole (construction) industry can be said to possess a culture (and, indeed, to the extent that such a diverse sector that represents almost 9% of GDP can be said to be a single industry), it is inevitably shaped by these forces.

This all makes for some very dismal reading, and it will be a matter of great interest and concern to see how, if at all, this Government, as well as future governments, respond.

For our part, we as design professionals have more than enough to do to get our own house in order, and in this respect, we will do well to take note of paragraph in which Morrell and Day remind us that:

‘products… (are developed)….. from raw materials (insulation for example) into a component (an insulated panel) into a system/assembly (cladding) and then into a completed building, with all of its systems and sub-systems, which must be built, commissioned, maintained and managed to serve its intended purpose.’

This again resonates with Dame Judith Hackitt’s view that building safety is contingent on safe systems. And here is the point: to date, with respect to the performance of buildings in conditions of fire, both the Approved Documents that provide guidance in terms of compliance with the Building Regulations, and the BBA test certificates upon which so much reliance has been placed by designers during product selection and specification, have placed far too much emphasis on the behaviour of discrete parts of buildings in isolation, rather than in the context of the ‘system’ or assembly of which they are but an isolated part.

That approach has been found to be as woefully lacking as it has been easily ‘gamed’ by manufacturers and suppliers whose interests and responsibilities stretch no further than maximising their market share and profit margins.

Thankfully, and not a moment too soon, their game is now up……. And if the Morrell and Day recommendations are adopted, those who design and specify buildings will find that the more comprehensive regulatory system recommended by Dame Judith will be complemented by a product testing and certification system that is easier to understand.

In terms of safe design and fitness for purpose can only be good news.